With 2023 well underway, it’s no secret that the medical professional liability (MPL) industry has faced and continues to face strong headwinds. In fact, rating agency AM Best notes that this insurance segment faces persistently depressed demand, rate adequacy concerns, rising loss costs and social inflation, diminishing reserve redundancies, and the potential for additional COVID-related claims frequency. Consequently, AM Best maintains a negative outlook for the MPL segment for this year.

Additionally, the industry has fallen behind other insurance lines in leveraging data and technology to improve underwriting efficiency, rating accuracy, and customer experience for agents, brokers, and insureds.

While you may have no control over many of the factors afflicting the industry, you do have control over technology and data. Within these new technologies and data analytical practices are many strategies and processes that make it much more feasible to understand better what your insureds are doing while automating underwriting. Through strategic automation, you can improve the accuracy of your premiums and claim projections while cutting costs through process improvements.

The Case for Automation in the MPL Industry

Automation sounds like a complex undertaking. Originally associated with the industrial revolution and auto manufacturing, automation conjures up images of assembly lines requiring years to change processes.

Fundamentally, insurance automation applies rules to data to inform decisions systematically with a minimum of human intervention. As with manufacturing, automation focuses human intelligence and expertise on decisions that add value.

Rising loss costs and social inflation are macro issues outside your underwriter’s control. Hence, superior underwriting should focus on rate adequacy, which encompasses evaluating risk accurately and pricing accordingly.

Superior data inform decisions about risk, leading to more consistent and profitable underwriting. Underwriting has always applied rules to available data. Previously, however, you had to rely on potentially unreliable self-reported data for premium underwriting. In contrast, you can gain access to vast datasets about medical procedures that provide access to vast datasets about medical procedures that shine a light on what your insureds and future insureds do every day. These powerful insights make it possible to automate underwriting to increase efficiency and improve results.

The ability to pre-populate forms accurately also enhances the experience for the agent, broker, and insured. Some carriers' applications are more than 10 pages, requiring excessive manual inputs and information from the provider or agent. This process introduces repetitive questions and human error. Automating the data feed reduces time and errors—time and energy that a provider typically doesn't have—and increases the likelihood that applications will be completed the first time. This, in turn, increases the conversion rate and improves the renewal rate.

Most MPL providers can relate to the pain points in the current manual application process. Automation addresses these pain points, creating a faster, easier, more accurate process that provides a competitive advantage. This approach worked for leading personal lines carriers that have taken a significant share from those who were slow to automate. Insurance programs for small businesses are following the same playbook, too.

Where to Start

That being said, automating renewal processing is the easiest entry point for automation. Because the medical professional or practice is a "known" commodity, the provider can evaluate changes in practice, physician turnover, and rate class consistency, plus malpractice history and recent claims, if any.

Underwriters receive alert reports three months before renewal. If the specialty matches the actual procedure's history, the renewal is typically processed. If not, it’s flagged for review.

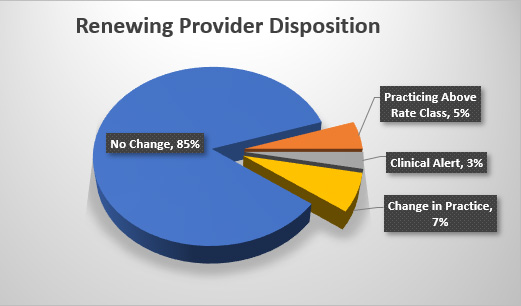

Research conducted by Preverity suggests that approximately 75 to 85% of medical providers have no significant change year over year. Underwriting should focus on the minority of providers that experienced a change.

- Has the doctor or practice expanded its services?

- Do they engage in higher-risk procedures?

- Does the doctor practice differently than other doctors in the same specialty?

Carriers can then apply a similar process to apply procedure-code analytics to prepopulate the application form. Applying the correct specialty drives accurate rating without human intervention, the first step to automating renewals. It also frees up underwriting resources to focus on new business.

Increasing Your Knowledge About Practice Scope

Underwriting typically assigns risk by specialty, a helpful proxy for potential risk. Yet evolving procedures and practice creep are known issues. For example, in 2017, 21% of general surgeons were doing bariatric procedures. This increased to more than 24% in 2021.1

In addition to uncovering practice creep, carriers must capture actual activity regardless of the specialty or subspecialty. Consider radiology. A radiologist connects the patient’s medical image to other examinations and tests, recommends further examinations or treatments, and talks with the referring doctor. Some radiologists, however, also treat diseases utilizing radiation oncology or minimally invasive, image-guided surgery. Interventional radiology includes angioplasty and stent placement, biopsy procedures, line and tube placement, uterine fibroid removal, and fluid drainage.

Not surprisingly, even “minimally invasive” radiology procedures are riskier than purely diagnostic x-rays or MRIs. The rate class for interventional radiologists can be double that of diagnostic radiologists because the event rates are approximately 50% higher.2 Yet the agent or underwriter can miss the distinction between diagnostic and interventional radiologists. It’s also possible to miss changes in procedures or the expansion of specialties. Because evolving medical procedures may not be captured, the MPL rating may not reflect the full impact of emerging risk factors.

Apply Big Data Insights to Drive Automation

How can carriers accelerate automation by applying superior data analytics to improve rate adequacy and improve customer experience?

There is a better way to capture a physician’s typical actions and associated risks. US health insurers require the reporting of procedure codes, billing, and prescribing activity. A number of companies, including Preverity, receive and analyze this real-time reporting. Just as ISO and AAIS develop rating factors based on the regulatory reporting they receive, Preverity uses reported data to model medical activity and associated risk. The data's quality, completeness, and improved latency, combined with advanced computing and industry insight, contribute to accurate classification.

Don’t Wait: Automate

Data-driven classification transformed personal lines and small business insurance. No carrier has the volume, variety, and velocity of data to go it alone. Carriers can now leverage advanced analytics to “get under the hood” and understand the risks taken by a doctor.

The MPL industry is poised to automate rate decision-making, focusing resources on opportunities to reduce risk and refine rates to deliver better underwriting results.

For MPL underwriters, early adopters will profit most because they will apply better selection, accurate rating, and accelerate automation in a shorter time. Early adopters can then tap into a virtuous cycle that begins with better data and superior selection leading to improved performance, which then leads to improved reinsurance terms. Finally, wins allow MPL automation leaders to pursue more and better-quality business.

References:

1. Preverity Study – Review of Procedure Codes, Billing and Prescribing activity from 2017 to 2021.

2. Preverity Study, above.